The modern-day lifestyle, unhealthy eating habits, stress, and unordered sleep cycle have increased the risk of health issues to a great extent. A critical illness can not only affect you physically and mentally but also devour the savings of a lifetime. Though illnesses may come unannounced, the best way to fight them is by being prepared. While suffering from a critical illness, one would like to resort to the best medical assistance without thinking about the burden of finance. Having a critical illness cover helps in gaining the financial security that you need in times of serious health issues. It is suggested to opt for a critical illness cover early in your life if you are at a significant risk of developing a critical illness. Let’s cover everything one must know and understand about critical illness covers in the UAE.

What is Critical Illness Cover?

A critical illness cover offers you financial protection against critical and potentially life-threatening diseases that require a hefty sum for treatment. Critical illness health insurance policies are designed to provide a lump-sum payout to the policyholder or any of the insured persons, in case they get diagnosed with a critical illness during the term of the policy. Having the right critical illness cover ensures safety and financial security against life-threatening ailments.

Health Insurance UAE Plans

Full Access

Dubai Insurance

Plan NameValue N4 (Remnto)

Medical Cover (AED)250,000

Starting FromAED 2,114/Yearly

NetworkDubai Care

Full Access

Cigna

Plan NameHealthguard Regional

Medical Cover (AED)2,750,000

Starting FromAED 11,634/Yearly

NetworkGeneral

Full Access

GIG Gulf (Previously AXA)

Plan NameGlobal

Medical Cover (AED)7,500,000

NetworkIn-house A1

GP Clinic

Takaful Emarat

Plan NameECARE BLUE

Medical Cover (AED)150,000

Starting FromAED 1,209/Yearly

NetworkE CARE Blue

Specialist Clinic

Orient Takaful Insurance

Plan NamePlan 5

Medical Cover (AED)1,000,000

Starting FromAED 1,561/Yearly

NetworkNEXTCARE RN3

Specialist Clinic

RAK Insurance

Plan NameNextcare RN3

Medical Cover (AED)1,000,000

Starting FromAED 1,617/Yearly

NetworkNEXTCARE RN3

Specialist Clinic

Orient Insurance

Plan NameHealth Plus - Plan 5

Medical Cover (AED)1,000,000

Starting FromAED 1,617/Yearly

NetworkNEXTCARE RN3

Specialist Clinic

Adamjee

Plan NameNAS WN

Medical Cover (AED)1,000,000

Starting FromAED 2,509/Yearly

NetworkNAS – WN (OP restricted to Clinics)

Full Access

Sukoon Bupa

Plan NameSelect

Medical Cover (AED)6,239,000

Starting FromAED 14,967/Yearly

NetworkPremium Network

Plans shown as per selected filters. T&Cs apply

Plans shown as per selected filters. T&Cs apply

What are the Benefits of Critical Illness Cover?

Having a critical illness cover is beneficial in a lot of ways. Some of the major benefits are:

Coverage Against Multiple Critical Illnesses: Most of the insurance plans with critical illnesses cover offer coverage against up to 38 critical illnesses.

Lump-Sum Coverage: One of the best advantages of critical illness plans is that the coverage is provided in the form of a lump-sum payout. It can be easily used as an income replacement in case the primary breadwinner of the family is sick or to cover the expenses of treatment.

Guaranteed Payout: If an insured member gets diagnosed with a critical illness during the tenure of the plan, a guaranteed lump sum payout is given out for the treatment of the affected or to cover the financial needs of the family members.

Easy Procedures: The process of application, approval, and claim settlement is easy and hassle-free which makes critical illness plans the right choice.

Enhanced Protection: Under the critical illness cover, an accidental death benefit may also be included, depending on the plan and providers. Check the details of all your top options and then choose the plan that provides the maximum protection at your preferred price.

Affordability: Most critical illness insurance plans in the UAE offer coverage with premium ranging between AED 200 and AED 2500. This makes critical illness plans an affordable way to secure the insured as well as the financial future of their family members.

What is Covered in Critical Illness Cover in UAE?

Not all critical illness health insurance uae plans cover all critical illnesses. However, highly comprehensive plans may cover up to 38 critical illnesses in the UAE. The following illnesses are generally covered under most critical illness covers:

Blindness, Loss of speech, Deafness – which is permanent and irreversible

Terminal illnesses like Cancer, AIDS, Diabetes, etc.

Coma – which has permanent symptoms

Dementia (including Alzheimer’s disease) and Parkinson's disease before age 65 – which results in permanent symptoms

Heart attack or Stroke– of specified severity

Kidney or Liver failure – that requires dialysis or in the last stage.

Loss or paralysis of hands or feet – permanent and irreversible

Lung disease – last stage/respiratory failure – of specified severity

Third-degree burns – that result in 20% of the body’s surface area affected or 50% of the face’s surface area affected

What is Not Covered in Critical Illness Cover in UAE?

While the critical illness cover is available against a wide range of diseases, it has some exclusions as well. It is always suggested to read the fine proof to confirm all the details. The exclusions under critical illness cover are:

Loss of the life of the insured by attempting suicide

The critical illness developed due to alcohol abuse, consumption of drugs, or illegal activities.

Accidents or diseases resulting from taking part in adventurous sports like trekking, mountain climbing, sky diving, etc.

Undergoing plastic surgery

Pre-existing diseases are not covered until the waiting period is over

How to Choose the Best Critical Illness Cover in UAE?

It is essential to compare the plans, check against a few standard metrics, and purchase the plan from a reliable insurance company to choose the best critical illness cover in the UAE. You must look out for the following features in a critical illness cover and choose the best one according to your requirements:

Coverage Extent: While investing in a critical illness plan, it is necessary to look out for the diseases which are covered under it and see if the match your requirements and exceptions.

Pre-existing and Chronic Conditions: Few insurance companies also offer coverage for treatment expenses for pre-existing and chronic diseases under the critical illness cover. However, all covers do not offer this benefit. Therefore, while choosing the critical illness cover verify with your insurance company if such a feature is available, in case you require the benefit.

Cost of the Critical Illness Cover: While choosing the critical illness cover in the UAE, compare the different price quotes by different companies and the features offered. Take into account the inclusions and exclusions of the plan. After that, whichever plan suits your requirements and budget the most, opt for it.

Best Critical Illness Cover in UAE:

Take a look at some of the best critical illness plans available in UAE, and pick the one that best suits your insurance needs as well as your budget:

Zurich Critical Illness Plan

Zurich Critical Illness Plan offers you protection against several life-threatening conditions. Here are some of its most striking features:

The plan offers 2 types of coverage:

Cancer Cover - that covers all types of cancer. In case of a cancer diagnosis, you will receive a cash payout.

Comprehensive Critical Illness Cover - that offers a payout in case one is diagnosed with any of the 34 listed illnesses of the plan.

The beneficiary of the policy receives funeral coverage of $5,000 without an extra charge.

Cancer cover/ critical illness cover is available for up to three children of the insured, as per the option selected. The offered coverage amount is $15,000 for each child.

Takaful Emarat - Silver

This comprehensive health insurance plan offers you worldwide health coverage along with an equally comprehensive critical illness cover. Following are a few details of the same:

It comes with an annual aggregate limit of AED 250,000.

Covers road ambulance expenses in case of an emergency.

Up to AED 5,000 coverage amount is allotted for prescribed medicines.

Chronic illnesses and pre-existing diseases are covered up to the annual limit.

The waiting period of 6 months is applicable for in-patient treatment of diabetes mellitus, cancer cases, neurosurgery, and arterial diseases.

Takaful Emarat - Rhodium

You can get the benefits of this comprehensive plan if you are an Abu Dhabi Visa Holder. Given below are a few key features of this comprehensive health insurance plan with critical illness cover:

The annual aggregate limit for this plan is AED 1 million.

You are eligible to get a Private room for your stay at the hospital.

The plan covers home nursing following your in-patient treatment for up to AED 7,500 a person.

Investigations and diagnoses are covered up to the annual limit.

Abu Dhabi National Insurance Company (ADNIC) - Shifa Bronze Opt 1

Let us take a look at some of the most important features of this plan:

The plan covers Semi-Private room type with a sub-limit of AED 400 per day.

Chronic and pre-existing conditions are covered under this plan.

X-Ray/ Lab and Scan are covered.

As an outpatient service, physiotherapy is also included.

Daman - Care Bronze DNE with Dental

Here are the best features of Daman Care Bronze DNE with a Dental plan and critical illness cover:

Pre-existing and chronic conditions are covered up to AED 150,000 provided they were declared on the Application Form.

Coverage is available in UAE only.

Out-Patient services include:

Laboratory tests with 10% coinsurance

Up to 15 sessions per year for physiotherapy treatment

Also offers coverage for alternative medicine

The yearly limit for medication is AED 10,000 per person.

In a nutshell

Critical illness treatment is costly so having a critical illness cover is always beneficial for financial security. Health insurance is essential for everybody living in the UAE. Employers in Dubai and Abu Dhabi offer mandatory health insurance coverage to their employees. However, having a separate or add-on critical illness cover can provide you with the extra protection you need. At Policybazaar UAE, you get to browse through a number of health insurance plans and compare their coverage and the premium to make an ideal choice. You can take your time to analyse each plan and make a well-informed decision.

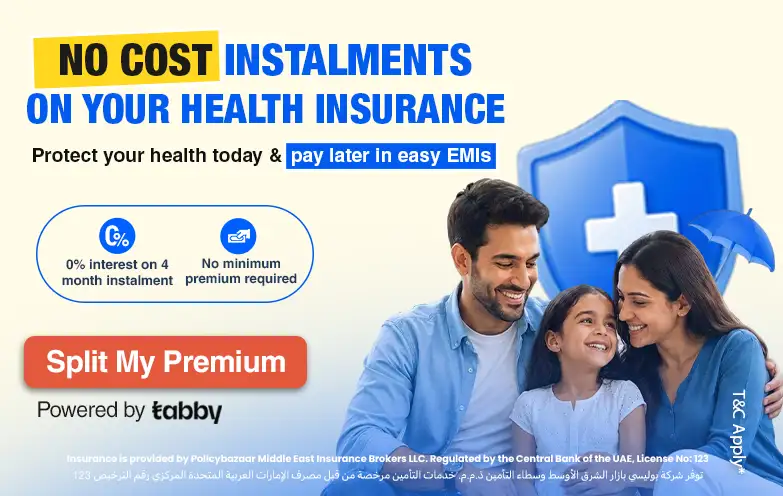

Last Updated : 17 Jun 2026Buy Insurance in Installments UAE | 0% Interest via TabbySplit your health or car insurance premium into 4 monthly payments at 0% interest with Tabby. No minimum premium. Coverage starts day one. Available at Policybazaar.ae.

Last Updated : 09 Jun 2026How to Boost Immunity in Children Naturally | UAEBoost your child's immunity naturally with proper sleep, balanced diet, daily exercise, and timely vaccinations - no supplements needed in most cases.

Last Updated : 09 Jun 2026Digital Detox: Why Your Brain Needs a Break from ScreensDigital detox is a regular break from screens that reduces stress, improves sleep quality, and boosts productivity. Learn the signs you need one and how to start.

Last Updated : 08 Jun 2026PCOS Officially Renamed PMOS – What It Means for WomenPCOS is now officially PMOS – Polyendocrine Metabolic Ovarian Syndrome. Learn what this landmark 2026 name change means for 170 million women worldwide.

Last Updated : 03 Jun 202620-Minute Workouts for Busy Professionals | Stay Fit Fast4 proven 20-minute workout routines for busy professionals. HIIT, strength, office-friendly & fat-burning cardio — stay fit without long gym sessions.

Last Updated : 03 Jun 2026Plant-Based Diet: Complete Guide to Benefits & FoodsA plant-based diet boosts heart health, weight loss, and immunity. Explore benefits, 5 food groups, and tips to get started in the UAE.

Last Updated : 10 Feb 2026How to Check Medical Insurance Status with Emirates ID?Emiratis will now be able to use their Emirates ID cards not only to go through immigration gates at the airport but to avail of medical services in the UAE.

Last Updated : 10 Jul 2026Best Health Insurance Companies in Dubai, UAE 2026Find the Top 10+ Health Insurance Companies in Dubai, UAE Offering Comprehensive Health Insurance Coverage and Exceptional Services at Affordable Prices.

Last Updated : 26 May 2026How to Check the Status of Your Health Insurance Online?The easiest way to get familiar with your plan details or check the active status is to do it online. Let’s figure out how to check if your health insurance plan is active online.

Last Updated : 08 Jan 2026Dental Insurance UAE: Dental Insurance Types, Coverage & BenefitsDental Insurance UAE: Know All about Dental Insurance, Types, Coverage & Benefits. Dental Insurance Covering Most of the Dental Treatments, You can Drop off Your Worries About Costly Therapies.

Last Updated : 11 Feb 2026Can You Buy Health Insurance for New Born Baby in UAE?Don't know whether you can buy medical insurance for new born baby in UAE? In this article we’ll share everything you need to know about health insurance for newborn baby.

Last Updated : 27 Nov 2025Where Can I Get Medical Help Without Having Health Insurance in UAE?Not everyone in the UAE can afford to buy a health insurance policy to avail of quality medical care benefits. To help out such people, we have listed here a few places and ways of getting medical help.

.png)

Last Updated : 17 Jun 2026Buy Insurance in Installments UAE | 0% Interest via TabbySplit your health or car insurance premium into 4 monthly payments at 0% interest with Tabby. No minimum premium. Coverage starts day one. Available at Policybazaar.ae.

Last Updated : 17 Jun 2026Buy Insurance in Installments UAE | 0% Interest via TabbySplit your health or car insurance premium into 4 monthly payments at 0% interest with Tabby. No minimum premium. Coverage starts day one. Available at Policybazaar.ae. Last Updated : 09 Jun 2026How to Boost Immunity in Children Naturally | UAEBoost your child's immunity naturally with proper sleep, balanced diet, daily exercise, and timely vaccinations - no supplements needed in most cases.

Last Updated : 09 Jun 2026How to Boost Immunity in Children Naturally | UAEBoost your child's immunity naturally with proper sleep, balanced diet, daily exercise, and timely vaccinations - no supplements needed in most cases. Last Updated : 09 Jun 2026Digital Detox: Why Your Brain Needs a Break from ScreensDigital detox is a regular break from screens that reduces stress, improves sleep quality, and boosts productivity. Learn the signs you need one and how to start.

Last Updated : 09 Jun 2026Digital Detox: Why Your Brain Needs a Break from ScreensDigital detox is a regular break from screens that reduces stress, improves sleep quality, and boosts productivity. Learn the signs you need one and how to start. Last Updated : 08 Jun 2026PCOS Officially Renamed PMOS – What It Means for WomenPCOS is now officially PMOS – Polyendocrine Metabolic Ovarian Syndrome. Learn what this landmark 2026 name change means for 170 million women worldwide.

Last Updated : 08 Jun 2026PCOS Officially Renamed PMOS – What It Means for WomenPCOS is now officially PMOS – Polyendocrine Metabolic Ovarian Syndrome. Learn what this landmark 2026 name change means for 170 million women worldwide.-(2)-(2).webp) Last Updated : 03 Jun 202620-Minute Workouts for Busy Professionals | Stay Fit Fast4 proven 20-minute workout routines for busy professionals. HIIT, strength, office-friendly & fat-burning cardio — stay fit without long gym sessions.

Last Updated : 03 Jun 202620-Minute Workouts for Busy Professionals | Stay Fit Fast4 proven 20-minute workout routines for busy professionals. HIIT, strength, office-friendly & fat-burning cardio — stay fit without long gym sessions.-(2).webp) Last Updated : 03 Jun 2026Plant-Based Diet: Complete Guide to Benefits & FoodsA plant-based diet boosts heart health, weight loss, and immunity. Explore benefits, 5 food groups, and tips to get started in the UAE.

Last Updated : 03 Jun 2026Plant-Based Diet: Complete Guide to Benefits & FoodsA plant-based diet boosts heart health, weight loss, and immunity. Explore benefits, 5 food groups, and tips to get started in the UAE. Last Updated : 10 Feb 2026How to Check Medical Insurance Status with Emirates ID?Emiratis will now be able to use their Emirates ID cards not only to go through immigration gates at the airport but to avail of medical services in the UAE.

Last Updated : 10 Feb 2026How to Check Medical Insurance Status with Emirates ID?Emiratis will now be able to use their Emirates ID cards not only to go through immigration gates at the airport but to avail of medical services in the UAE. Last Updated : 10 Jul 2026Best Health Insurance Companies in Dubai, UAE 2026Find the Top 10+ Health Insurance Companies in Dubai, UAE Offering Comprehensive Health Insurance Coverage and Exceptional Services at Affordable Prices.

Last Updated : 10 Jul 2026Best Health Insurance Companies in Dubai, UAE 2026Find the Top 10+ Health Insurance Companies in Dubai, UAE Offering Comprehensive Health Insurance Coverage and Exceptional Services at Affordable Prices. Last Updated : 26 May 2026How to Check the Status of Your Health Insurance Online?The easiest way to get familiar with your plan details or check the active status is to do it online. Let’s figure out how to check if your health insurance plan is active online.

Last Updated : 26 May 2026How to Check the Status of Your Health Insurance Online?The easiest way to get familiar with your plan details or check the active status is to do it online. Let’s figure out how to check if your health insurance plan is active online. Last Updated : 08 Jan 2026Dental Insurance UAE: Dental Insurance Types, Coverage & BenefitsDental Insurance UAE: Know All about Dental Insurance, Types, Coverage & Benefits. Dental Insurance Covering Most of the Dental Treatments, You can Drop off Your Worries About Costly Therapies.

Last Updated : 08 Jan 2026Dental Insurance UAE: Dental Insurance Types, Coverage & BenefitsDental Insurance UAE: Know All about Dental Insurance, Types, Coverage & Benefits. Dental Insurance Covering Most of the Dental Treatments, You can Drop off Your Worries About Costly Therapies. Last Updated : 11 Feb 2026Can You Buy Health Insurance for New Born Baby in UAE?Don't know whether you can buy medical insurance for new born baby in UAE? In this article we’ll share everything you need to know about health insurance for newborn baby.

Last Updated : 11 Feb 2026Can You Buy Health Insurance for New Born Baby in UAE?Don't know whether you can buy medical insurance for new born baby in UAE? In this article we’ll share everything you need to know about health insurance for newborn baby. Last Updated : 27 Nov 2025Where Can I Get Medical Help Without Having Health Insurance in UAE?Not everyone in the UAE can afford to buy a health insurance policy to avail of quality medical care benefits. To help out such people, we have listed here a few places and ways of getting medical help.

Last Updated : 27 Nov 2025Where Can I Get Medical Help Without Having Health Insurance in UAE?Not everyone in the UAE can afford to buy a health insurance policy to avail of quality medical care benefits. To help out such people, we have listed here a few places and ways of getting medical help.