How to Claim If You Have Multiple Health Insurance Plans in UAE

“Health is wealth!” As a result, all of us should make efforts to safeguard this wealth at all costs. This is where health insurance enters the picture. Health insurance is a necessity for our lives today. With the ever-increasing medical costs and the escalating health risks that catch us prey, it is important to get insured medically.

The insurance industry is full of health insurance plans but unfortunately, that makes it overwhelmingly confusing. One common question that arises in a person’s mind when they want to buy a health insurance cover is whether it is possible to buy more than one health insurance policy to cover their medical expenses?

Health Insurance UAE Plans

GP Clinic

HAYAH Insurance

Plan NameNRI Care Blue

Medical Cover (AED)250,000

Starting FromAED 1,101/Yearly

NetworkE CARE Blue

GP Clinic

Dubai Insurance

Plan NameEcare Blue

Medical Cover (AED)1,000,000

Starting FromAED 1,455/Yearly

NetworkE CARE Blue

Full Access

Abu Dhabi National Insurance Company

Plan NameBronze

Medical Cover (AED)250,000

Starting FromAED 3,178/Yearly

NetworkMSHI Bronze

Full Access

Cigna

Plan NameHealthguard Regional

Medical Cover (AED)2,750,000

Starting FromAED 11,457/Yearly

NetworkGeneral

Full Access

GIG Gulf (Previously AXA)

Plan NameGlobal

Medical Cover (AED)7,500,000

NetworkIn-house A1

GP Clinic

Fidelity United

Plan NameHealth First Plan G

Medical Cover (AED)1,000,000

Starting FromAED 1,175/Yearly

NetworkPCP- C Network

GP Clinic

Takaful Emarat

Plan NameECARE BLUE

Medical Cover (AED)150,000

Starting FromAED 1,209/Yearly

NetworkE CARE Blue

Specialist Clinic

RAK Insurance

Plan NameNextcare RN3

Medical Cover (AED)1,000,000

Starting FromAED 1,390/Yearly

NetworkNEXTCARE RN3

Specialist Clinic

Orient Takaful Insurance

Plan NamePlan 5

Medical Cover (AED)1,000,000

Starting FromAED 1,561/Yearly

NetworkNEXTCARE RN3

Specialist Clinic

Orient Insurance

Plan NameHealth Plus - Plan 5

Medical Cover (AED)1,000,000

Starting FromAED 1,617/Yearly

NetworkNEXTCARE RN3

Specialist Clinic

Adamjee

Plan NameNAS WN

Medical Cover (AED)1,000,000

Starting FromAED 2,509/Yearly

NetworkNAS – WN (OP restricted to Clinics)

Full Access

Sukoon Bupa

Plan NameSelect

Medical Cover (AED)6,239,000

Starting FromAED 14,465/Yearly

NetworkPremium Network

Plans shown as per selected filters. T&Cs apply

Plans shown as per selected filters. T&Cs apply

Mandatory Health Insurance in the UAE

The government of the United Arab Emirates has made health insurance mandatory for its residents. As a consequence, employers in the region are required to offer health coverage to their employees and their families while every sponsor has to provide a health insurance plan to their resident dependents. The strict UAE laws state that failure to abide by this rule can attract a fine of AED 500 per month. Furthermore, alongside the fine, no new visas will be issued and none of the existing visas will be renewed without health insurance Dubai as per the Dubai Health Authority. This could however pose a problem if the resident already has health insurance that gives additional coverage beyond the group medical insurance offered by the employer. Alternatively, one might even have an existing policy, and getting a second insurance cover to get higher coverage might seem logical. For instance, a resident’s wife has a health cover provided by her spouse’s employer. If she takes up a job where her new employer is obligated by law to offer her a health insurance policy. The question arises- will both insurance cards work or if they are to be used interchangeably?

Dubai Health Authority (DHA) on multiple Health Insurance Plans

According to the Dubai Health Authority, the premier government authority overlooking the health system in Dubai, there is no restriction on the number of health insurance plans availed by a resident. The law only demands that every resident is covered by at least one health insurance policy and no rules are violated by owning multiple health insurance covers. However, if an individual can reap the benefits of multiple insurances depends entirely on the agreement between the employer and their resident employee. Some employers might insist that the benefits of health insurance are applicable only if the employee has no other health insurance policies covering their medical costs.

Furthermore, the DHA mandates that it is okay to have two health insurance plans concurrently however a resident can only make a claim from anyone's policy, thus making double claims illegal. One also needs to separately submit the documents in order to make a claim.

Unfortunately, this is not as simple as it sounds. Insurance providers seek to transfer the liability for any loss onto the other insurer. Insurers in the UAE are notorious for doing this since they know that once another insurance provider has satisfied the liability, they are no longer obligated to settle the claim or contribute to covering the medical expenses. There are two reasons for this:

The UAE laws prohibit a policyholder from getting more than the value of the loss. AS such if the health coverage offered by the first insurer covers the loss and for subjective reasons if the policyholder chooses to make the claim only against that particular insurer then the policyholder has no more incentives to claim against the loss from the second insurer. AS seen in most cases, the policyholder is often not even aware that they are entitled to get coverage for the loss under the second health insurance policy.

As soon as the loss is fully indemnified under the first insurer’s policy, the laws in UAE do not give any rights to the first insurer to sue the other insurers who are equally liable for the loss to make a contribution to the claim.

In many countries, the decision for insurers to contribute rose out of equity. It is not a right that is recognized by the law. While in many other countries the right exists due to legislation. If it has not been devised by legislation, as in the United Arab Emirates, this right is not available.

Regardless of whether the right to contribute is legally available in a country or not, this condition is required for a claim to contribution in the case of multiple insurances.

Multiple insurance or dual insurance takes place when one part is insured by two or more insurance providers with respect to the same issue and the same interest as well as against the same risk and for a similar period of time. Each of these specific elements has to be present for it to be considered dual insurance.

Mentioned underneath the cases where dual insurance claims usually take place:

A project involving construction that includes a ‘Construction All Risks’ policy. This ensures that the contractor and the subcontractor are insured in case of personal injury and property damage. Usually, the subcontractor already carries his own public liability insurance. In the unfortunate event where the subcontractor incurs a liability for personal injury, both the health insurance plans will respond, barring an exclusion.

A motor vehicle accident that causes the driver personal injury. Generally, the driver has motor vehicle insurance alongside the employer’s compensation insurance both of which are liable for the driver’s injury except for when there is a provision in either of the health insurance policies stating otherwise.

In the healthcare sector, medical practitioners who are hired as independent contractors by hospitals tend to have their own professional liability insurance cover. They might also fall under the professional liability coverage of the hospital that retains them. This is a common phenomenon across the UAE and the GCC.

In any of the above-mentioned circumstances, if there is loss or damage by any of the risks insured against, then as per the terms of each policy, the person insured or the entity insured might be liable to receive the full sum of the loss from any of the insurance provider or insurance providers that they choose to claim it from.

What are some of the other insurance provisions?

Due to the fact that the UAE does not allow insurers paying for a claim any right of contribution from the other insurance providers who are also equally liable for the loss, the insurance companies operating in the UAE deal pre-emptively with the cases of dual health insurance plans through the policy wordings. Some of the commonly used policy wordings with respect to dual insurance are:

Rateable Proportion Clauses: Such clauses are incorporated so as to protect the insurer from claims of full losses against the health insurance policies of the insured. This clause states that each insurance provider will be liable only for a rateable proportion of the claim. Let’s take an example of this clause to understand it better- “If under this policy any claim arises when at the time there is an existing insurance covering the same damages or liabilities, the insurance provider shall not be held liable for paying or contributing more than the rateable proportion of any damage, loss, compensation or expense.”

Notification Clauses: This clause provides that unless the policyholder gives written notice to the policy provider about the existence of other health insurance plans covering the same risk, the policy will remain void. An example of such a clause is- “ No claim will be recoverable if the person insured is previously insured elsewhere unless the particulars of any such insurance have been notified in writing to the insurer.”

Excess Clauses: Such clauses convert the health insurance policies having them into an excess insurance policy such that the coverage is only triggered in the event where the loss exceeds the limit of the additional insurance held by the insured. Here is an example of the clause- “If at the time of the occurrence of damage, loss or injury there exists another insurance or indemnity wholly or partially covering the same damage, loss or injury, the insurance provider will not be held liable to contribute or pay towards such damage, loss or injury except in excess of the sum recovered or recoverable under any other insurance or indemnity.”

In a Nutshell

In the absence of a UAE law for an independent right of contribution between insurers, policy providers pre-emptively change their policy wordings. It is therefore important to carefully read the policy terms and conditions while browsing through health insurance plans in the UAE.

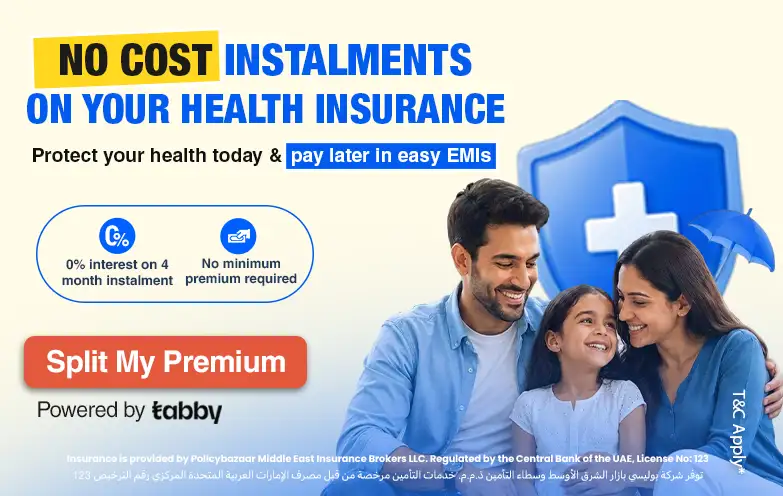

Last Updated : 17 Jun 2026Buy Insurance in Installments UAE | 0% Interest via TabbySplit your health or car insurance premium into 4 monthly payments at 0% interest with Tabby. No minimum premium. Coverage starts day one. Available at Policybazaar.ae.

Last Updated : 09 Jun 2026How to Boost Immunity in Children Naturally | UAEBoost your child's immunity naturally with proper sleep, balanced diet, daily exercise, and timely vaccinations - no supplements needed in most cases.

Last Updated : 09 Jun 2026Digital Detox: Why Your Brain Needs a Break from ScreensDigital detox is a regular break from screens that reduces stress, improves sleep quality, and boosts productivity. Learn the signs you need one and how to start.

Last Updated : 08 Jun 2026PCOS Officially Renamed PMOS – What It Means for WomenPCOS is now officially PMOS – Polyendocrine Metabolic Ovarian Syndrome. Learn what this landmark 2026 name change means for 170 million women worldwide.

Last Updated : 03 Jun 202620-Minute Workouts for Busy Professionals | Stay Fit Fast4 proven 20-minute workout routines for busy professionals. HIIT, strength, office-friendly & fat-burning cardio — stay fit without long gym sessions.

Last Updated : 03 Jun 2026Plant-Based Diet: Complete Guide to Benefits & FoodsA plant-based diet boosts heart health, weight loss, and immunity. Explore benefits, 5 food groups, and tips to get started in the UAE.

Last Updated : 10 Feb 2026How to Check Medical Insurance Status with Emirates ID?Emiratis will now be able to use their Emirates ID cards not only to go through immigration gates at the airport but to avail of medical services in the UAE.

Last Updated : 08 Jul 2026Best Health Insurance Companies in Dubai, UAE 2026Find the Top 10+ Health Insurance Companies in Dubai, UAE Offering Comprehensive Health Insurance Coverage and Exceptional Services at Affordable Prices.

Last Updated : 26 May 2026How to Check the Status of Your Health Insurance Online?The easiest way to get familiar with your plan details or check the active status is to do it online. Let’s figure out how to check if your health insurance plan is active online.

Last Updated : 08 Jan 2026Dental Insurance UAE: Dental Insurance Types, Coverage & BenefitsDental Insurance UAE: Know All about Dental Insurance, Types, Coverage & Benefits. Dental Insurance Covering Most of the Dental Treatments, You can Drop off Your Worries About Costly Therapies.

Last Updated : 11 Feb 2026Can You Buy Health Insurance for New Born Baby in UAE?Don't know whether you can buy medical insurance for new born baby in UAE? In this article we’ll share everything you need to know about health insurance for newborn baby.

Last Updated : 27 Nov 2025Where Can I Get Medical Help Without Having Health Insurance in UAE?Not everyone in the UAE can afford to buy a health insurance policy to avail of quality medical care benefits. To help out such people, we have listed here a few places and ways of getting medical help.

.png)

Last Updated : 17 Jun 2026Buy Insurance in Installments UAE | 0% Interest via TabbySplit your health or car insurance premium into 4 monthly payments at 0% interest with Tabby. No minimum premium. Coverage starts day one. Available at Policybazaar.ae.

Last Updated : 17 Jun 2026Buy Insurance in Installments UAE | 0% Interest via TabbySplit your health or car insurance premium into 4 monthly payments at 0% interest with Tabby. No minimum premium. Coverage starts day one. Available at Policybazaar.ae. Last Updated : 09 Jun 2026How to Boost Immunity in Children Naturally | UAEBoost your child's immunity naturally with proper sleep, balanced diet, daily exercise, and timely vaccinations - no supplements needed in most cases.

Last Updated : 09 Jun 2026How to Boost Immunity in Children Naturally | UAEBoost your child's immunity naturally with proper sleep, balanced diet, daily exercise, and timely vaccinations - no supplements needed in most cases. Last Updated : 09 Jun 2026Digital Detox: Why Your Brain Needs a Break from ScreensDigital detox is a regular break from screens that reduces stress, improves sleep quality, and boosts productivity. Learn the signs you need one and how to start.

Last Updated : 09 Jun 2026Digital Detox: Why Your Brain Needs a Break from ScreensDigital detox is a regular break from screens that reduces stress, improves sleep quality, and boosts productivity. Learn the signs you need one and how to start. Last Updated : 08 Jun 2026PCOS Officially Renamed PMOS – What It Means for WomenPCOS is now officially PMOS – Polyendocrine Metabolic Ovarian Syndrome. Learn what this landmark 2026 name change means for 170 million women worldwide.

Last Updated : 08 Jun 2026PCOS Officially Renamed PMOS – What It Means for WomenPCOS is now officially PMOS – Polyendocrine Metabolic Ovarian Syndrome. Learn what this landmark 2026 name change means for 170 million women worldwide.-(2)-(2).webp) Last Updated : 03 Jun 202620-Minute Workouts for Busy Professionals | Stay Fit Fast4 proven 20-minute workout routines for busy professionals. HIIT, strength, office-friendly & fat-burning cardio — stay fit without long gym sessions.

Last Updated : 03 Jun 202620-Minute Workouts for Busy Professionals | Stay Fit Fast4 proven 20-minute workout routines for busy professionals. HIIT, strength, office-friendly & fat-burning cardio — stay fit without long gym sessions.-(2).webp) Last Updated : 03 Jun 2026Plant-Based Diet: Complete Guide to Benefits & FoodsA plant-based diet boosts heart health, weight loss, and immunity. Explore benefits, 5 food groups, and tips to get started in the UAE.

Last Updated : 03 Jun 2026Plant-Based Diet: Complete Guide to Benefits & FoodsA plant-based diet boosts heart health, weight loss, and immunity. Explore benefits, 5 food groups, and tips to get started in the UAE. Last Updated : 10 Feb 2026How to Check Medical Insurance Status with Emirates ID?Emiratis will now be able to use their Emirates ID cards not only to go through immigration gates at the airport but to avail of medical services in the UAE.

Last Updated : 10 Feb 2026How to Check Medical Insurance Status with Emirates ID?Emiratis will now be able to use their Emirates ID cards not only to go through immigration gates at the airport but to avail of medical services in the UAE. Last Updated : 08 Jul 2026Best Health Insurance Companies in Dubai, UAE 2026Find the Top 10+ Health Insurance Companies in Dubai, UAE Offering Comprehensive Health Insurance Coverage and Exceptional Services at Affordable Prices.

Last Updated : 08 Jul 2026Best Health Insurance Companies in Dubai, UAE 2026Find the Top 10+ Health Insurance Companies in Dubai, UAE Offering Comprehensive Health Insurance Coverage and Exceptional Services at Affordable Prices. Last Updated : 26 May 2026How to Check the Status of Your Health Insurance Online?The easiest way to get familiar with your plan details or check the active status is to do it online. Let’s figure out how to check if your health insurance plan is active online.

Last Updated : 26 May 2026How to Check the Status of Your Health Insurance Online?The easiest way to get familiar with your plan details or check the active status is to do it online. Let’s figure out how to check if your health insurance plan is active online. Last Updated : 08 Jan 2026Dental Insurance UAE: Dental Insurance Types, Coverage & BenefitsDental Insurance UAE: Know All about Dental Insurance, Types, Coverage & Benefits. Dental Insurance Covering Most of the Dental Treatments, You can Drop off Your Worries About Costly Therapies.

Last Updated : 08 Jan 2026Dental Insurance UAE: Dental Insurance Types, Coverage & BenefitsDental Insurance UAE: Know All about Dental Insurance, Types, Coverage & Benefits. Dental Insurance Covering Most of the Dental Treatments, You can Drop off Your Worries About Costly Therapies. Last Updated : 11 Feb 2026Can You Buy Health Insurance for New Born Baby in UAE?Don't know whether you can buy medical insurance for new born baby in UAE? In this article we’ll share everything you need to know about health insurance for newborn baby.

Last Updated : 11 Feb 2026Can You Buy Health Insurance for New Born Baby in UAE?Don't know whether you can buy medical insurance for new born baby in UAE? In this article we’ll share everything you need to know about health insurance for newborn baby. Last Updated : 27 Nov 2025Where Can I Get Medical Help Without Having Health Insurance in UAE?Not everyone in the UAE can afford to buy a health insurance policy to avail of quality medical care benefits. To help out such people, we have listed here a few places and ways of getting medical help.

Last Updated : 27 Nov 2025Where Can I Get Medical Help Without Having Health Insurance in UAE?Not everyone in the UAE can afford to buy a health insurance policy to avail of quality medical care benefits. To help out such people, we have listed here a few places and ways of getting medical help.